Memo: Ninety-Nine Percent of Drone Defence Startups Will Die, But What About Europe?

Ninety-nine percent of drone companies will die. That's the prediction from Anduril's Chief Business Officer Matthew Steckman, made on a recent podcast. Of the 10,000 drone companies operating today, only a hundred would survive.

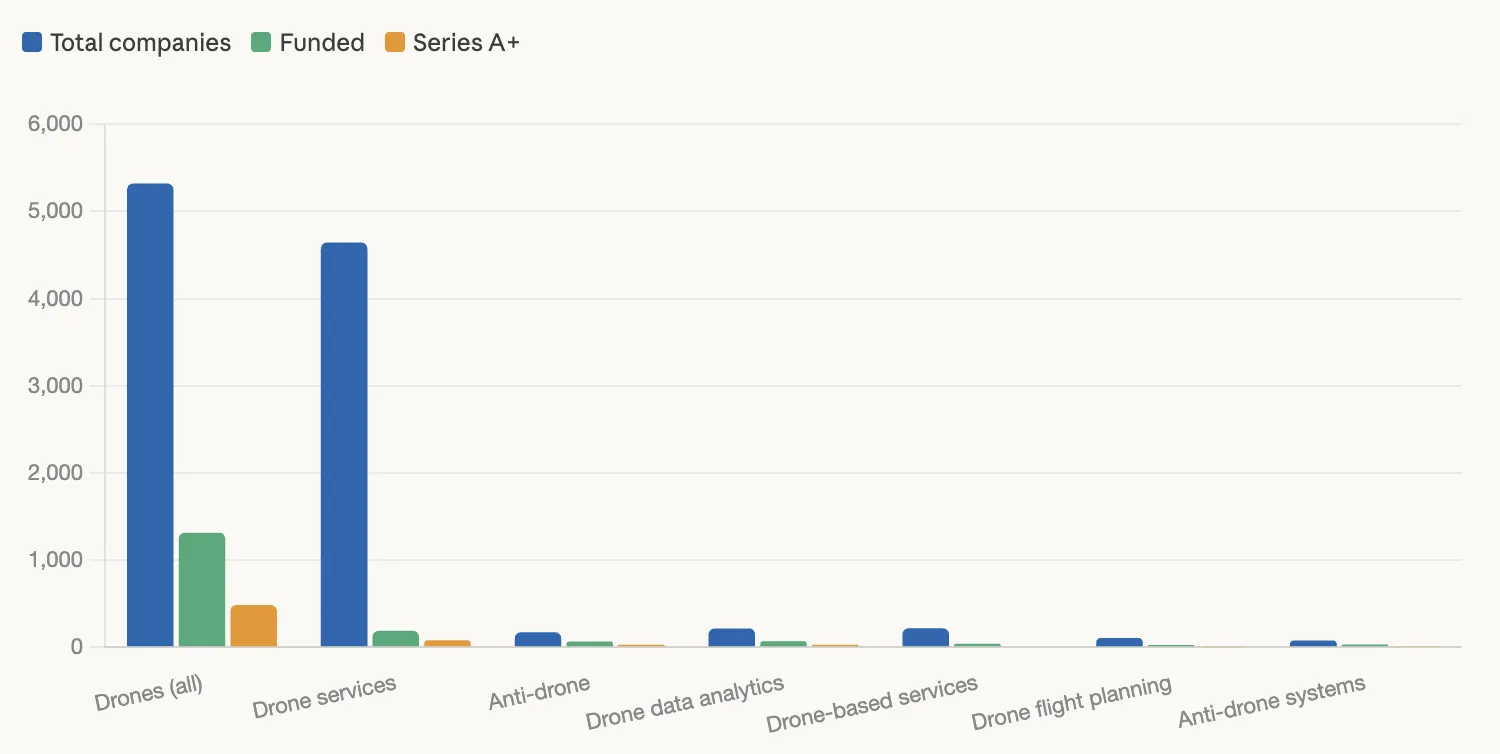

The global drone market at the end of 2025. Source: Tracxn/Failory via Anthropic.

There are currently seven drone unicorns: Anduril, Helsing, DJI, Zipline, Quantum Systems, Shield AI, and Skydio. Five are heavily focused on defence, unsurprising, given where the funding is flowing. The anti-drone segment remains small, with just 176 companies, but counter-drone funding surged 2,300% last year, reflecting the radical shift in how modern warfare has been waged in Ukraine.

Steckman's prediction is easier to defend in the U.S., where defence contracting flows from a single customer. Anduril's $20 billion order earlier this month appears to have settled that market, and the recent Palantir government exclusivity deal alongside a new $60 billion valuation cements its dominant position. The Thielverse has secured the future of U.S. defence. Europe is only beginning to reckon with what that means.

U.S. venture capital has done its work. The retail market, meanwhile, is just waking up. Swarmer AI, a Ukraine-tested startup with only $350,000 in prior orders, surged 1,200% in its first 48 hours of trading, a reflection of how scarce and coveted public defence technology plays have become.

But, as always, Europe is different.

Europe Is Not One Market, It's Three

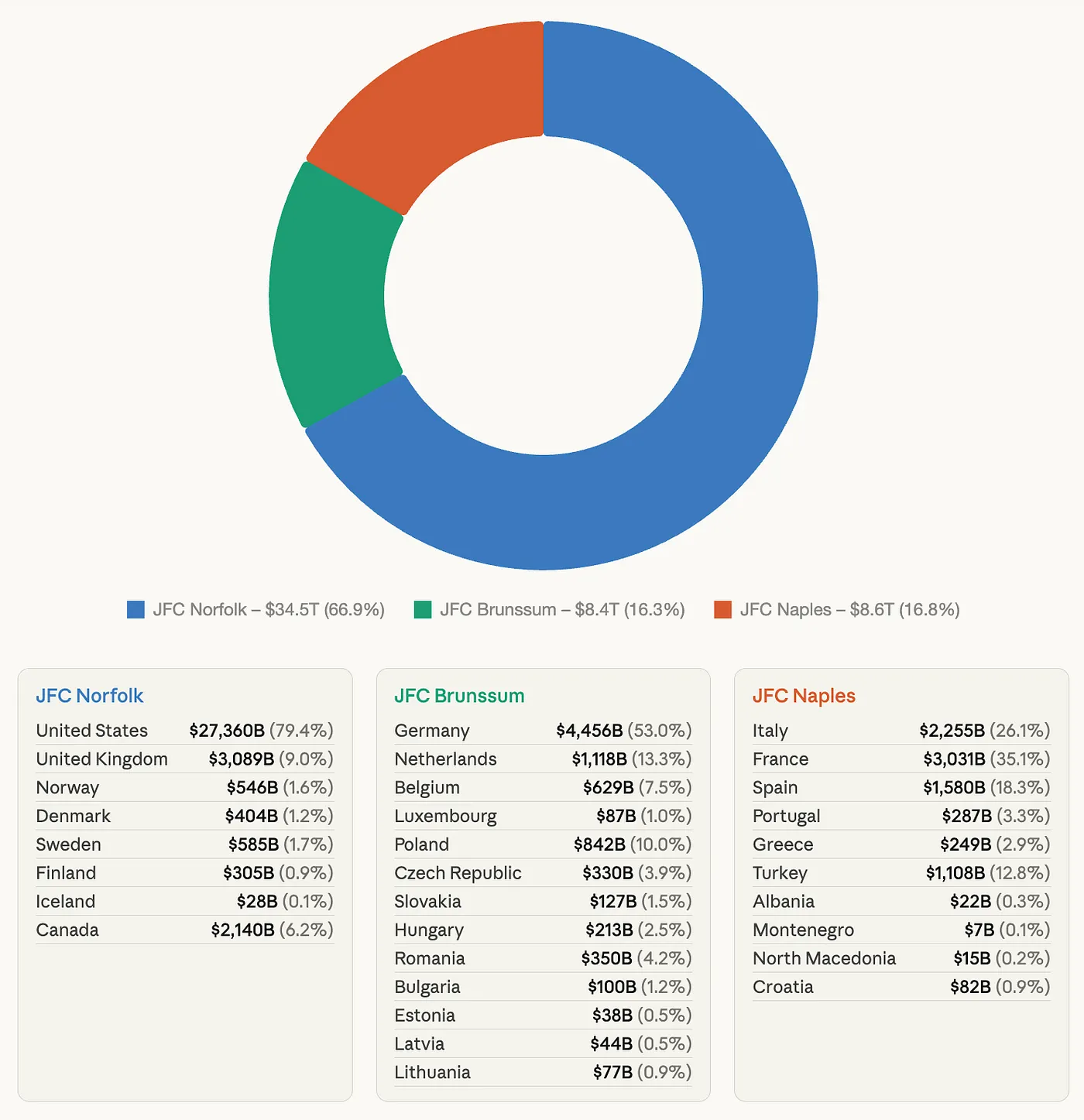

A significant transatlantic defence decision went largely unnoticed this February when the U.K. was handed control of NATO's Joint Force Command in Norfolk, Virginia, the nerve centre of NATO's Arctic defence covering the U.K., Denmark, Finland, Iceland, Norway, and Sweden.

The significance runs deeper than it appears. The "Europeanization of NATO" is quietly producing distinct regional enclaves. The Northern countries are consolidating around JFC Norfolk and a closer U.S. relationship. Italy, Greece, Turkey, Spain, Portugal, and the Balkans fall under JFC Naples, forming a separate Mediterranean naval cluster. And JFC Brunssum holds Europe's Eastern flank except for Finland's 1,340km border with Russia, which answers to Norfolk. Half of Europe's Russian front reports to the Netherlands, the other half to Virginia. One is becoming more European, the other more transatlantically aligned creating a contracting conundrum.

The result is that European NATO operates across at least three distinct spheres of influence. Unlike the U.S. Department of War, there is no single procurement customer just different European groupings with different sizes, threat perceptions and political temperaments.

The three JFC’s by GDP. Sources: NATO, IMF, World Bank via Anthropic.

Tier 1 defence investors have noticed. Despite rising defence budgets across the continent, money isn't flowing freely into European defence tech. The direction is set, but the destination isn't. Germany's recent cap on defence tech spending per company has already caused turbulence at Helsing and Stark, both backed by U.S. investors. An early sign of how unpredictable investing in European procurement can be.

It's increasingly plausible that Europe will fragment into three distinct drone defence markets. Two distinctly European and volatile, one more transatlantically coupled and stable.

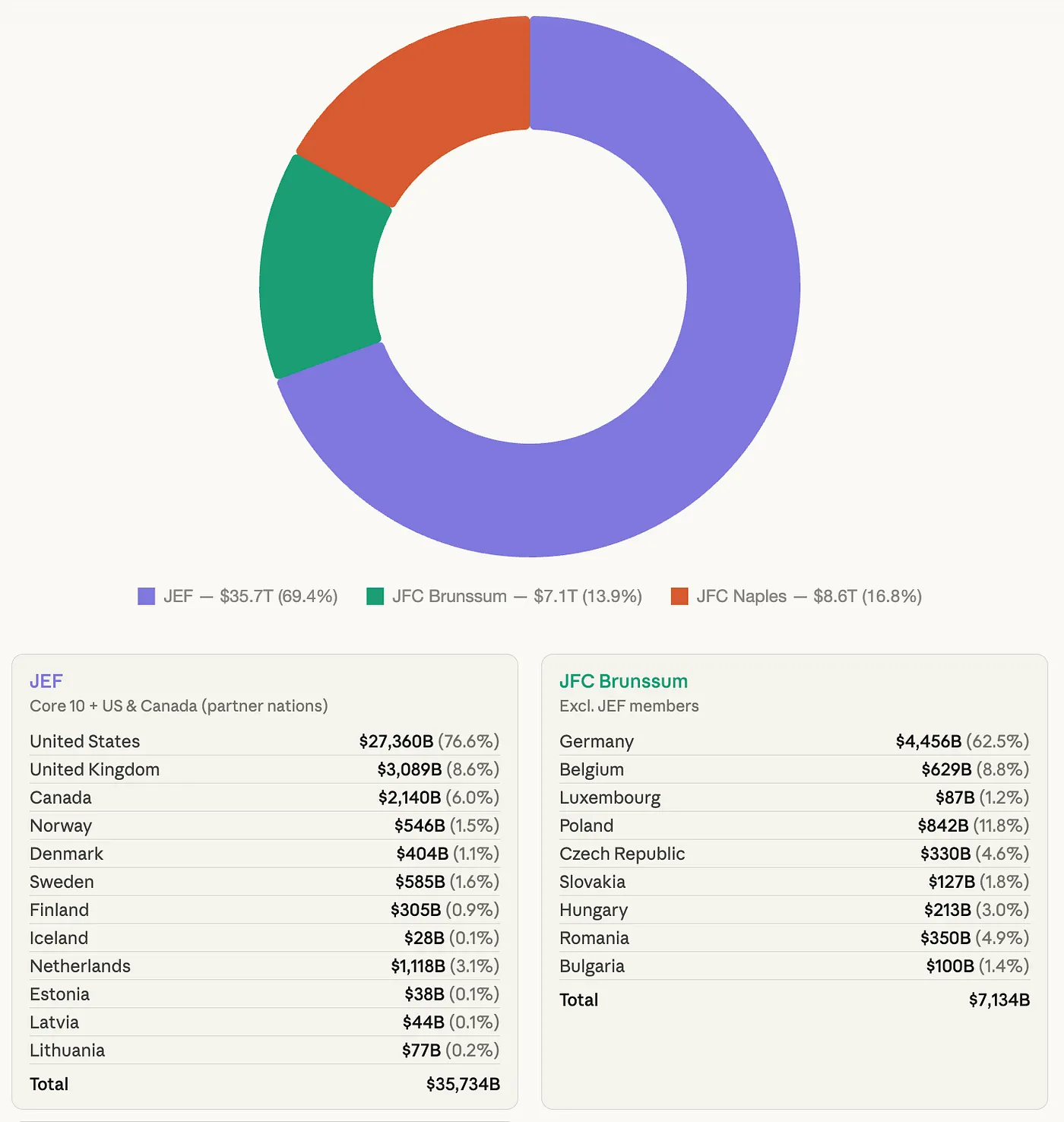

The Joint Expeditionary Force

Europe is experiencing its greatest upheaval since the Cold War, squeezed between a grinding war in Ukraine and mounting pressure from its most powerful ally. Against this backdrop, one European defence grouping is actually moving, the Joint Expeditionary Force.

JEF is the driving force behind Baltic Sentry, designed to protect Baltic Sea infrastructure from further sabotage. With roughly 40% of Russian oil transiting the Baltic, this initiative carries U.S. interest as well. Factor in the Arctic dimension and JEF would represent around 69% of NATO's total budget.

Poland's potential accession would extend the alliance's reach to the Suwalki Gap, Russia's land corridor to Kaliningrad, effectively denying Russian access to the southern Baltic. JEF's coherence is also notable for what it excludes, volatile members like Hungary and Slovakia are absent, making consensus more achievable.

JEF vs the JFC’s by GDP. Sources: NATO, IMF, World Bank via Anthropic.

Because JEF is moving fastest, it may generate the first real procurement demand. It also comprises the countries least encumbered by legacy defence industry, which makes them more open to the kind of new-model defence technology that startups can actually provide.

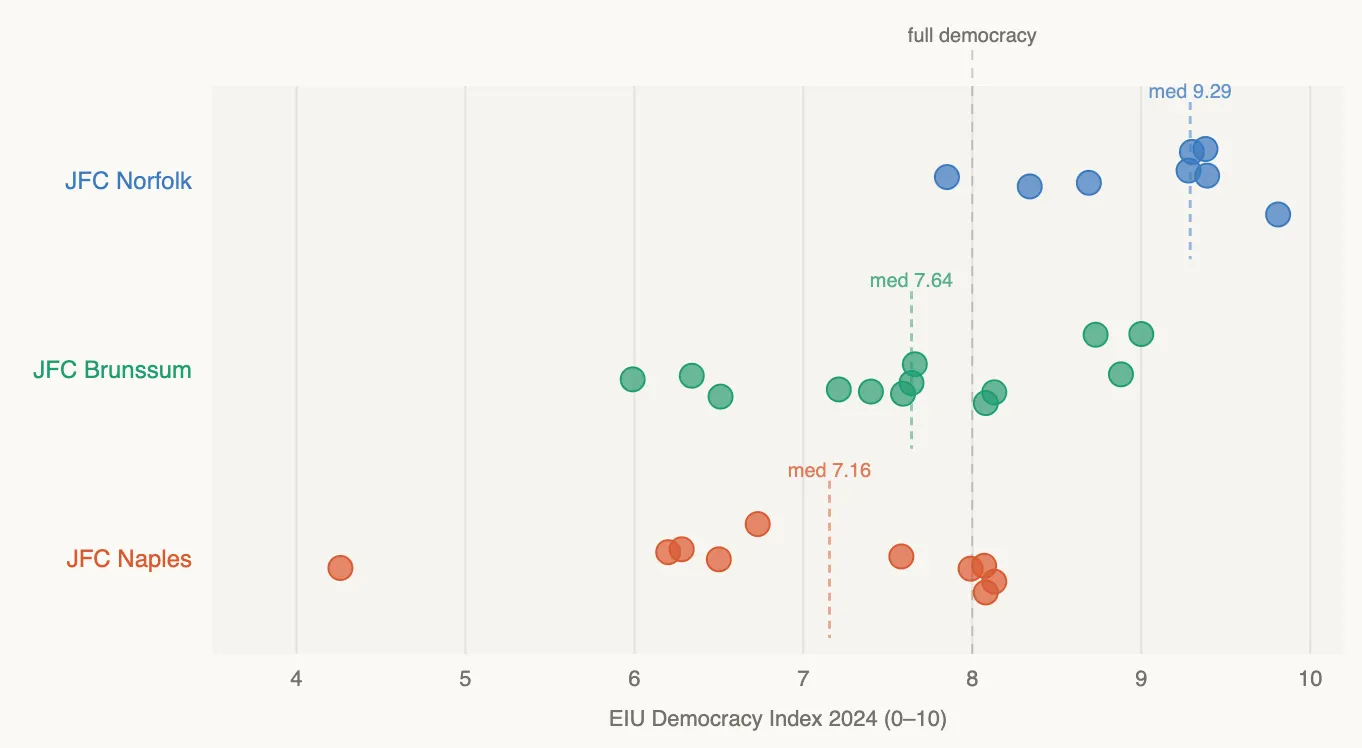

Democracy, Cohesion, and Who Moves First

Even as the U.S. pulls back from European defence broadly, one strategic interest keeps it engaged. The Arctic. The countries aligned with that interest — the Nordics and the U.K. — are, by design or coincidence, the same nations in JFC Norfolk.

The democratic character of the three commands is telling. JFC Norfolk is the only one composed entirely of full democracies with the U.S. itself falling just below that threshold, yet still above the averages of both Brunssum and Naples. More significantly, Norfolk's democracy scores cluster tightly, suggesting stronger internal cohesion. That cohesion is likely to translate into faster, cleaner procurement decisions.

Democracy levels of the three JFCs. Source: Economist, NATO, IMF via Anthropic.

Stark's recent decision to open offices in Stockholm, as it struggles with Germany's spending cap, signals that at least some companies are already repositioning toward the Arctic enclave.

The economic architecture of each command also matters. Both Norfolk and Brunssum are anchored by a dominant economy, the U.S. and Germany, respectively, while Naples is more evenly distributed across three larger nations. Poland, one of Europe's fastest-growing economies, is deepening its defence build-up rapidly while the Baltic states, with a combined GDP one-fifth of Poland's, are starting almost from scratch.

Founders and investors are caught in this geopolitical centrifuge. The most agile will find the seams between these enclaves and adjust. And none of this yet accounts for the future of the European Union itself, which the current U.S. administration appears intent on fracturing, using its deepening involvement in Iran as an off-ramp out of NATO commitments entirely.

The Middle East Wildcard

If Europe's complexity weren't enough, the Iran crisis is further destabilising the transatlantic relationship while simultaneously opening new doors for some. Defence companies with the right profiles may find themselves well positioned to attract investment and orders from Saudi Arabia, the UAE, and Qatar.

With U.S. stockpiles reportedly running low, a window may be opening for European suppliers to meet Middle Eastern demand. France has historically played this role, but this cycle the preference is likely to favour suppliers with stronger U.S. ties, assuming the Abraham Accords and the Board of Peace hold.

JFC Naples might seem the natural candidate, but it shows little sign of producing what the region needs, Turkish technology aside. The more credible contender is JFC Norfolk. The U.K. and the Nordics, whose U.S. alignment makes them more trusted partners and whose industrial capacity Washington would likely prefer to develop anyway, as part of its broader Arctic production strategy.

The U.S. defence technology market may be settled. The European market is far from it. The startups that can navigate both, and potentially the Middle East as well, will access the largest pools of capital and the most attractive exits. While cap table structures matter more as the U.S.-EU rift widens, the evolution of the Joint Force Commands may turn out to be the clearest map of where European new defence contracting is actually headed.